Real Estate Financing Tutorial: Secure Strategic Success

Finding the right capital structure for real estate projects is rarely simple. Market conditions in major cities like Denver or Miami require strategies that fit local realities, not a generic solution. Assessing project requirements and investment goals is the starting point for profitable and sustainable outcomes. This guide offers clear steps for structuring deals, securing funding, and building the foundation for financial resilience, whether you are seeking institutional, private equity, or sustainable investment across diverse regions.

Table of Contents

- Step 1: Assess Project Requirements And Investment Goals

- Step 2: Structure Entities And Negotiate Financing Terms

- Step 3: Conduct Thorough Financial Due Diligence

- Step 4: Optimize Deal Structuring And Secure Capital

- Step 5: Verify Funding Approval And Begin Project Execution

Quick Summary

| Key Insight | Explanation |

|---|---|

| 1. Assess Project Requirements | Understand physical and operational scopes to align with financing options and investor expectations. |

| 2. Structure Entities Carefully | Choose the right legal entity to help manage liability and optimize tax benefits based on your situation. |

| 3. Conduct Thorough Due Diligence | Review financial documents meticulously to uncover potential issues that could affect profitability. |

| 4. Optimize Capital Structure | Develop a well-balanced capital stack that suits your project’s financial profile and risk level. |

| 5. Verify Funding Approval | Ensure all funding agreements are legally binding and conditions are met before project execution begins. |

Step 1: Assess Project Requirements and Investment Goals

Before you commit capital or negotiate financing terms, you need clarity on what your project actually demands and where you want it to go. This assessment forms the foundation for every decision that follows, from choosing the right financing structure to identifying partners who align with your vision. You cannot secure the right capital if you do not understand what you are building and why.

Start by documenting the physical and operational scope of your project. What are you building, renovating, or repositioning? Calculate the total development cost broken down by phase: land acquisition, construction labor, materials, permits, infrastructure, and contingencies. Be honest about timelines. A 24-month construction schedule requires different financing than a 36-month build. Consider your project’s location and what makes it viable there. Market fundamentals in suburban Denver differ dramatically from those in downtown Miami or secondary markets in emerging regions. Understanding finance options across different geographic contexts helps you match your capital structure to local economic conditions rather than forcing a one-size-fits-all approach.

Next, define your investment objectives with specificity. Are you maximizing cash-on-cash returns over the next three years? Building a long-term hold with stable income? Creating a value-add opportunity that generates a 25 percent IRR over five years? Each objective changes how you structure debt, equity, and operational milestones. If sustainability and green building certifications matter to your investment thesis, your project requirements expand to include environmental compliance and long-term energy performance targets. Green financing principles for sustainable real estate connect your environmental goals directly to your financing strategy, helping you attract capital that values resilience alongside returns.

Align your project requirements with your operational capacity. Can your team manage a complex renovation while coordinating with contractors and municipal agencies? Are you comfortable holding a property through a market downturn, or do you need exit flexibility in your financing terms? Be realistic about what your organization can execute. Mismatch between project complexity and team capability creates delays, cost overruns, and stress that no amount of capital can solve. Your financing partner should understand these operational realities and help you structure deals that match your actual bandwidth, not your aspirational bandwidth.

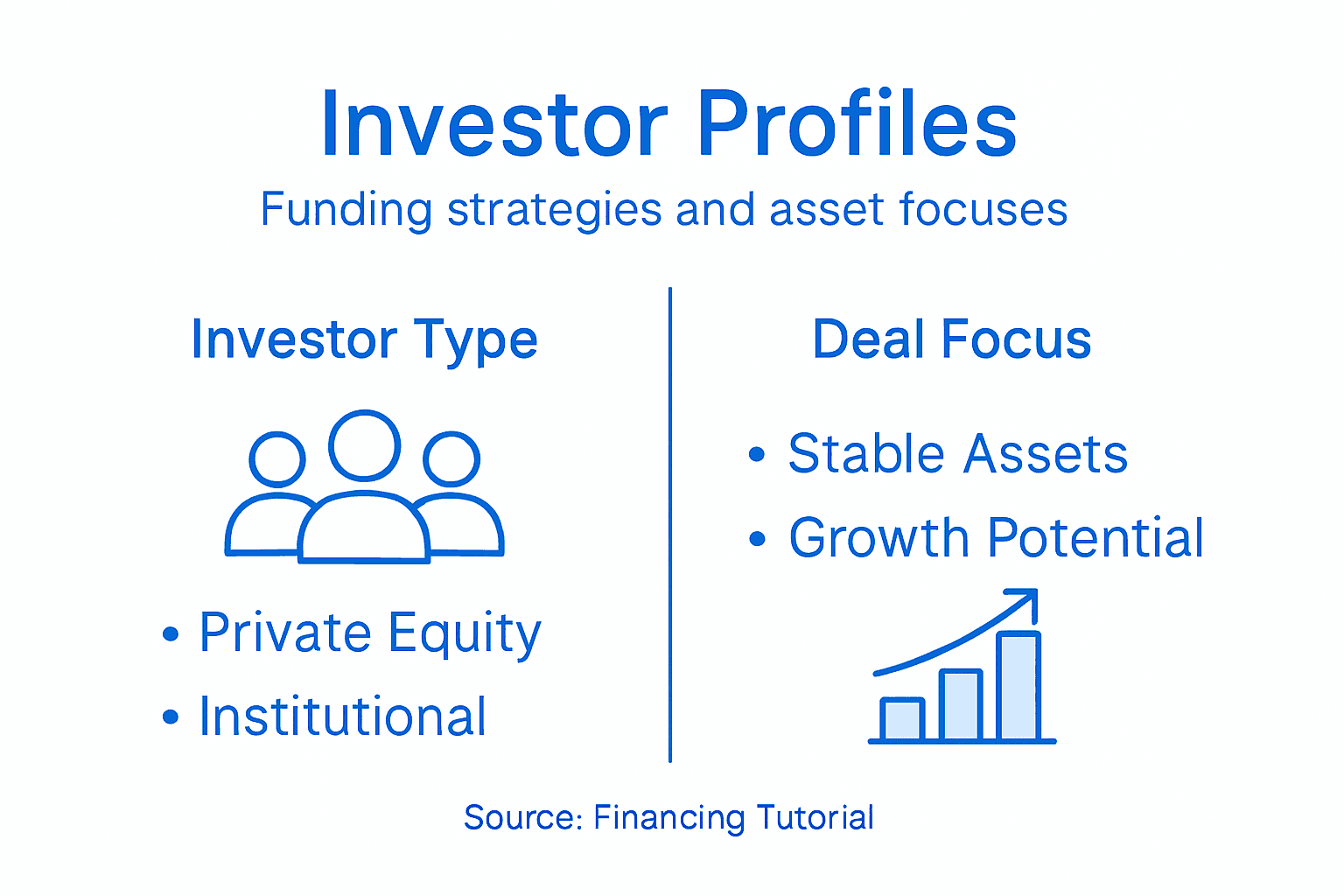

Finally, identify how your project attracts capital. Does it appeal to institutional investors looking for stable multifamily income? Construction lenders seeking projects with strong presales or predetermined exit timelines? Sustainable investment funds prioritizing ESG criteria? Different investor profiles have different requirements, timelines, and risk tolerances. Know your audience early because it shapes everything from your underwriting assumptions to your exit strategy.

Here’s a summary of common investor types and the capital they typically seek in real estate projects:

| Investor Type | Preferred Asset Class | Capital Requirements | Typical Deal Focus |

|---|---|---|---|

| Institutional Investor | Multifamily/Commercial | Stable cash flow | Long-term income |

| Construction Lender | Development/New builds | Presales, exit strategy | Short-term project completion |

| Sustainable Fund | Green-certified properties | ESG criteria, resilience | Environmental returns plus profit |

| Private Equity Partner | Value-add/redevelopment | Aggressive upside | High IRR, flexible structures |

Pro tip: Document your project requirements and investment goals in a single-page summary before meeting with any financing partner. This clarity prevents endless conversations and signals that you have done your homework, which accelerates the lending decision and gives you stronger negotiating leverage.

Step 2: Structure Entities and Negotiate Financing Terms

Your entity structure and financing terms determine how much control you retain, what your tax obligations look like, and whether your deal survives when market conditions shift. These are not administrative afterthoughts. They are strategic decisions that require intentional negotiation and legal precision before you sign anything binding.

Start with entity structuring. Most real estate investors operate through some form of limited liability company or partnership, but the right structure depends on your specific situation. Are you investing solo or with partners? How do you want to handle liability protection? What are your tax objectives? A single property might live in its own LLC separate from your other holdings, giving you liability compartmentalization. A portfolio of rental properties might benefit from different structuring than a development project with multiple equity partners and construction lenders. The entity structure affects which financing products you qualify for, how lenders view your application, and what happens if something goes wrong on one project. Work with a real estate attorney and accountant before you finalize your legal structure. Get it wrong and you could face unexpected tax bills, liability exposure, or financing complications years later.

Once your entity is established, you move to financing term negotiation. Traditional bank loans come with standardized terms that feel rigid, but creative financing structures offer flexibility you would not find with institutional lenders. Understanding negotiation strategies across different financing methods reveals how seller financing, owner financing, and wrap around mortgages give you leverage to customize payment schedules, interest rates, down payments, and exit timelines. The key is knowing what matters most to your lender and what flexibility exists within that framework. Some lenders prioritize monthly cash flow. Others want principal paid down rapidly. Some accept longer construction timelines. Others need projects closed within twelve months. Your job is to understand their motivations and structure terms that satisfy their requirements while protecting your interests.

Negotiation requires you to come prepared with specificity. Do not walk into a conversation saying “I need favorable terms.” Instead, bring clear numbers. What loan amount do you need? What interest rate have you modeled? What repayment schedule aligns with your projected cash flow? What happens if market conditions delay your refinance or sale? When you specify terms with precision, you signal that you understand your deal and you are serious about executing. Vague requests signal uncertainty and weakness. Lenders respond to confidence backed by data.

Be prepared to accept that some terms are negotiable and others are fixed based on lender requirements or market conditions. Interest rates often have less flexibility than amortization schedules or prepayment penalties. Down payments might be non negotiable while loan covenants could have room to move. Identify early which terms truly matter to your deal success and which are secondary. You cannot win everything. Prioritize strategically.

Documentation is where good deals become enforceable agreements. Proper legal instruments like promissory notes and binding agreements protect both you and your lender by specifying exactly what happens under different scenarios. What triggers a default? What happens if you miss a payment? What are your remedies if the lender violates the agreement? These are not theoretical questions. When stress emerges, clarity in your documents prevents costly disputes. Have an attorney draft or review all financing documents before execution.

Pro tip: Create a one page term sheet that outlines your proposed financing structure before any official negotiation begins. This forces you to think through key variables and gives lenders a clear framework to evaluate quickly, which accelerates their decision and prevents endless back and forth conversations.

Step 3: Conduct Thorough Financial Due Diligence

Financial due diligence separates deals that look profitable on a spreadsheet from deals that actually generate returns. This is where you verify the story the seller told you, challenge assumptions you built into your models, and uncover the financial realities hiding in the details. Skip this step or rush through it and you will buy problems instead of properties.

Start by requesting complete financial documentation from the seller or current owner. You need three years of tax returns, profit and loss statements, rent rolls showing every tenant and lease term, utility bills, insurance policies, maintenance records, and property management agreements. Do not accept summaries or highlights. Request the actual documents. Summaries hide inconvenient details. When you see the raw records, patterns emerge. Are certain units consistently vacant? Have utility costs spiked in the past year? Are maintenance expenses concentrated in specific systems that may need replacement soon? Comprehensive financial verification uncovers hidden issues and verifies income reliability before you commit capital. Early detection of financial red flags gives you negotiation leverage or the information you need to walk away entirely.

Analyze income streams with skepticism. The rent roll shows what tenants pay, but does that income actually materialize? Review bank deposits against the rent roll to verify collections match claims. Calculate occupancy rates for the past three years. If a property shows 95 percent occupancy in the seller’s financial statements but actual collections show 78 percent, you have discovered a major discrepancy. Ask why. Is the market soft? Is the property in decline? Are management practices weak? Each answer changes your underwriting. Review lease terms to understand when income might change. Tenants on month to month arrangements create income uncertainty. Triple net leases where tenants pay their own expenses look different than gross leases where the property owner covers everything. Know exactly what income you are actually buying and what uncertainty surrounds that income stream.

Scrutinize expense categories with equal intensity. Operating expenses include property taxes, insurance, utilities, maintenance, management fees, and repairs. Compare current year expenses against the previous two years and against industry benchmarks for similar properties in your market. Are expenses trending up or down? Sudden increases in utilities, repairs, or maintenance suggest deferred problems coming due soon. If the property has not replaced the roof in fifteen years and the roof typically lasts twenty years, you are buying a roof replacement that will cost thirty to fifty thousand dollars within the next few years. That is not an opportunity. That is a bill you are inheriting. Speak with the property manager and maintenance team to understand what systems are aging, what will need replacement or major repair in the next five years, and what capital expenditures are already planned. This shifts your financial model from optimistic assumptions to grounded reality.

Examine insurance coverage and tax payment history. Under insurance creates liability exposure. Lenders require specific coverage levels and will walk away if policies are inadequate. Verify that property taxes are current and paid in full. Delinquent tax payments can trigger foreclosure proceedings independent of mortgage defaults. Review any disputes, assessments, or planned reassessments that might increase your tax burden. One property we evaluated faced a five percent reassessment that would have increased annual taxes by forty two hundred dollars. The seller had not disclosed this pending reassessment. Catching this during due diligence changed our offer price significantly.

Work with an accountant or financial analyst who understands real estate if you are analyzing complex properties with multiple units, commercial components, or unusual structures. Their trained eye will catch patterns and inconsistencies that untrained analysis misses. The cost of professional analysis is minimal compared to the cost of buying a property with hidden financial problems. Complete your financial due diligence before you commit to a purchase price. This is not negotiable.

Pro tip: Create a standardized financial analysis template that you use for every property you evaluate. This forces consistency in your analysis process and makes it easy to compare opportunities side by side without missing critical variables or falling into the trap of analyzing similar deals differently based on emotional attachment.

Step 4: Optimize Deal Structuring and Secure Capital

The difference between a deal that barely works and a deal that generates exceptional returns often comes down to how you structure your capital stack. Strategic deal structuring unlocks efficiency, reduces your risk exposure, and attracts the right capital sources for your specific project. This is where financial engineering meets real estate execution.

Understand the capital stack as a hierarchy of claims on your property or project. At the base sits senior debt, which gets paid first and carries the lowest risk and lowest return. Above that sits mezzanine debt, which ranks behind senior lenders but ahead of equity holders. Then comes preferred equity, which receives preferential returns before common equity holders. At the top sits common equity, your investment, which bears the most risk but captures upside above agreed return thresholds. Balancing these financing layers across risk and return profiles optimizes how much leverage you can deploy while maintaining financing flexibility and lender confidence. A properly structured capital stack attracts diverse funding sources because each layer gets appropriate risk adjusted returns.

Start by defining your project’s financial profile. What is your total project cost? What timeline do you have? What is your exit strategy and expected return? These factors determine how much leverage you can responsibly take and what combination of financing layers makes sense. A stabilized rental property generating predictable cash flow can typically support sixty to seventy percent debt to value. A development project with construction risk and an uncertain exit can only support thirty to forty five percent debt to value. Trying to force higher leverage than your project can support simply transfers risk to lenders who will ultimately demand higher interest rates and more restrictive covenants. That overhead kills your returns. Underleverage your deal and you leave capital efficiency on the table. Your job is finding the optimal leverage point where you maximize returns without creating financial stress.

Once you know your leverage target, determine which capital layers make sense for your deal. Maybe your deal qualifies for senior bank debt at competitive rates. That should form your foundation because it is the cheapest capital available. If you need more leverage, mezzanine debt fills the gap between senior debt and equity. Mezzanine lenders accept higher risk than senior lenders but want lower returns than equity investors. If you have patient capital from partners or investors accepting lower returns in exchange for downside protection, preferred equity provides that stability without the covenant restrictions that come with debt. Common equity sits at the top and captures the upside once other investors receive their contracted returns.

Compare how the major capital stack layers differ in structure and risk:

| Layer | Repayment Priority | Risk Level | Expected Return |

|---|---|---|---|

| Senior Debt | First | Lowest | Fixed interest rate |

| Mezzanine Debt | After senior debt | Moderate | Higher interest rate |

| Preferred Equity | Before common equity | Medium | Preferred dividends |

| Common Equity | Last | Highest | Capital appreciation |

Securing capital at each layer requires understanding what each investor profile actually wants. Senior lenders want certainty. They want experienced sponsors, strong cash flow, real collateral, and a clear path to repayment. Construction lenders want project controls and experienced general contractors who execute on time and budget. Mezzanine investors want visibility into operations and some control over major decisions. Equity partners want transparent reporting and confidence in the operator. Speak directly with potential capital sources early in your process. Understand their investment criteria, their return requirements, their timeline, and their deal structure preferences. This intelligence lets you design a capital stack that attracts capital instead of repelling it.

Document your capital structure with precision in your financing agreements. Specify payment hierarchies, return waterfalls, refinancing rights, default triggers, and exit procedures. Ambiguity creates disputes when markets shift or deals underperform. Clarity prevents expensive conflicts. Have your attorney review all capital structure documents before execution. The cost of legal precision is negligible compared to the cost of capital structure disputes down the road.

Pro tip: Model three different capital stack scenarios for your deal: conservative, moderate, and aggressive leverage. Show each scenario to potential lenders and equity partners to gauge their comfort levels before you commit to a specific structure, ensuring you can actually secure the capital at terms that work for your deal.

Step 5: Verify Funding Approval and Begin Project Execution

Funding approval marks the moment when your deal transforms from negotiation into action. Before you break ground, order materials, or deploy your team, you must verify that all funding commitments are legally binding, all conditions have been satisfied, and capital will actually flow when you need it. This verification step prevents costly delays and ensures your project timeline stays on track.

Start by confirming that all funding agreements are fully executed and legally binding. Your loan documents, equity commitments, and any mezzanine financing arrangements need to be signed by all parties with proper authority. Do not assume verbal confirmations constitute binding commitments. Ensuring legal agreements and financial commitments are secured among all parties protects your project and prevents financing gaps from emerging during construction. Have your attorney confirm that all documentation is complete and meets lender and investor requirements. Review the conditions precedent in your financing agreements. These are the requirements you must satisfy before lenders will release funds. Typical conditions include proof of construction insurance, evidence that permits are in place, confirmation that you have hired your general contractor, and verification that your equity capital is deposited in escrow. Some lenders require environmental clearances or title insurance commitments. Know exactly which conditions apply to your deal and create a checklist to track completion. Missing a single condition precedent can delay fund drawdowns by weeks or months.

Verify the fund draw schedule and disbursement procedures. Real estate financing does not typically arrive in a single lump sum. Instead, funds disburse in phases tied to construction milestones or project stages. Your loan agreement specifies when draws occur, how much is available at each draw, and what documentation is required to trigger each disbursement. Typical construction loans disburse funds as work progresses, with lenders requiring proof that prior draws were spent properly and that construction is progressing on schedule. Understand these procedures intimately because delays in obtaining approvals for draws can starve your project of cash and create schedule pressure. Before construction starts, work with your lender to establish a draw schedule that aligns with your construction timeline. Get written approval for your anticipated draw dates. This prevents surprises and allows your project team to plan financing needs with confidence.

Confirm that all regulatory approvals and permits are secured. Building permits, environmental clearances, zoning approvals, and any specialized licenses required for your project must be in place before construction begins. Lenders typically will not release construction funds until permits are issued. If your project requires multiple permits or approvals, start the application process early. Permitting delays are common and can cascade into financing and construction delays. Create a permitting checklist and assign responsibility for each approval. Track progress weekly and escalate any delays immediately. One month of permitting delays can cost you tens of thousands of dollars in financing costs and construction crew availability.

Ensure that your general contractor, subcontractors, and insurance are in place before you request the initial draw. Your lender requires proof that you have hired a qualified general contractor experienced with your project type. They want to see lien waivers from all major subcontractors confirming they have been paid for prior work. They require certificates of insurance showing that your project is properly covered against liability, property damage, and worker injury. These requirements exist because lenders protect their collateral. The last thing they want is a project disrupted by contractor disputes, unpaid liens, or insurance gaps. Get all of this documentation organized and ready to submit before you request your first draw.

Financial close represents the moment when complete funding is secured and capital is available for drawdown. This is your green light to begin construction. Once you reach financial close, your project transitions from planning mode into execution mode. Your focus shifts from securing capital to managing construction, controlling costs, maintaining schedule, and reporting to lenders and equity investors. This is where operational discipline matters most. Projects that execute well maintain lender confidence and keep financing relationships strong for future deals. Projects that stumble face scrutiny, increased oversight, and potential financing complications.

Pro tip: Create a comprehensive closing checklist that tracks every condition precedent, permit, insurance requirement, and lender approval needed before the first draw. Assign responsibility for each item, establish target completion dates two weeks before you plan to request funds, and conduct a final verification meeting with your lender one week before closing to confirm all conditions are satisfied.

Unlock Strategic Success in Real Estate Financing with Sims Ventures

Navigating the complexities of real estate financing requires more than just capital. As this tutorial highlights, mastering entity structuring, negotiating clear financing terms, and rigorous due diligence can determine your project’s outcome. Many investors face challenges such as aligning capital stacks, meeting lender conditions, and managing post-closing requirements. At Sims Ventures, we understand these critical pain points and provide comprehensive support that transforms these challenges into opportunities for growth.

Our partnership approach means you receive expert guidance on structuring your deal and capital stack while accessing innovative financing solutions tailored to your goals. Whether you are optimizing your investment return, managing operational risks, or securing stable funding, our team stands ready to help every step of the way. Learn how to maximize your investment potential by exploring Real Estate Investment: Maximize Your Profits.

Take control of your real estate journey today. Visit Sims Ventures for strategic advisory combined with flexible financing designed specifically for your success. Don’t let critical financing decisions delay your next project. Connect with us now to secure the capital and expertise you need to execute with confidence.

Frequently Asked Questions

What are the key steps in securing financing for a real estate project?

Before securing financing, assess your project requirements, entity structure, and investment goals. Document the total development cost and align your objectives with your operational capacity to create a solid foundation for financing discussions.

How can I ensure my financing terms align with my project’s goals?

Negotiate your financing terms by clearly defining your project’s financial profile, including expected returns and the level of risk you’re willing to accept. Prioritize which terms truly matter to the success of your deal to ensure favorable negotiating outcomes.

What financial documents should I request during due diligence?

Request three years of tax returns, profit and loss statements, rent rolls, utility bills, and maintenance records from the seller. Verify these documents to uncover any hidden issues that could affect your investment.

How do I optimize my capital stack when structuring a deal?

Start by determining your total project cost, desired exit strategy, and risk tolerance to create the right mix of senior debt, mezzanine debt, and equity. Model different capital stack scenarios to understand which combination will attract the best financing terms for your project.

What should I verify before starting my real estate project?

Ensure all funding commitments are legally binding and all conditions precedent have been satisfied before starting the project. Create a checklist to track necessary permits, insurance, and regulatory approvals to avoid costly delays.

How can I prepare for lender meetings effectively?

Document your project requirements and financial needs in a one-page summary before meeting with potential lenders. This preparation will provide clear insights and demonstrate that you are serious about your financing needs, helping to accelerate the lending decision.

{kind=link}