Real Estate Syndication: Unlocking Bigger Deals Together

Every serious investor has faced this problem: top-tier commercial properties often remain out of reach when acting alone. Real estate syndication bridges this gap, letting multiple investors pool resources for deals once reserved for large institutions. With a sponsor managing acquisitions and operations, and investors enjoying passive ownership with defined protections, this approach delivers professional management, diversified exposure, and a single path toward accessing high-value American real estate projects.

Table of Contents

- Real Estate Syndication Explained in Plain Terms

- Key Players and Structuring Models

- Profit Distribution Models

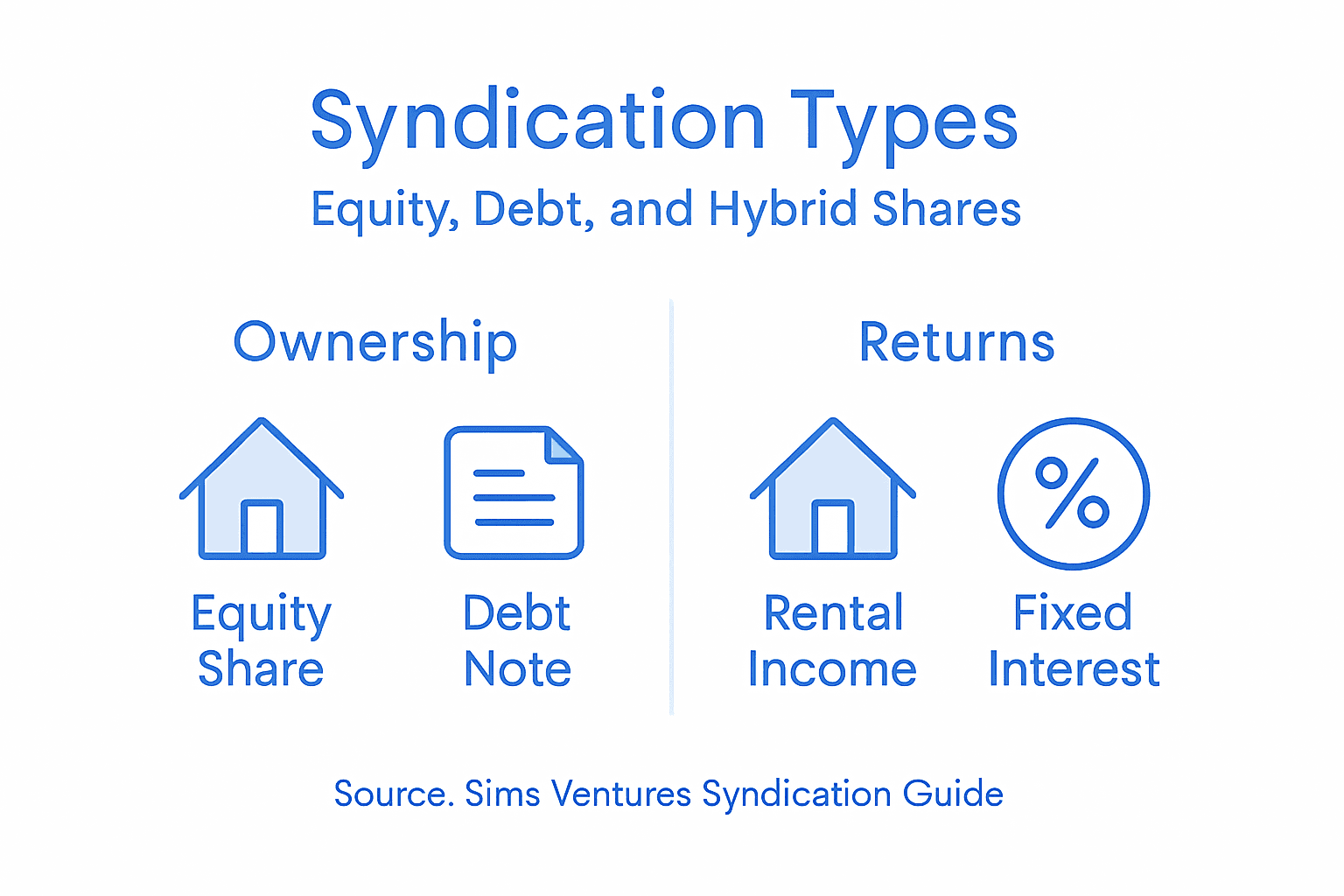

- Types: Equity, Debt, and Hybrid Syndications

- Step-by-Step Deal Process and Payouts

- Legal Framework, Disclosure, and Compliance Rules

- Risks, Common Pitfalls, and Exit Considerations

Key Takeaways

| Point | Details |

|---|---|

| Real Estate Syndication Structure | Syndication pools capital from multiple investors to acquire large properties, managed by a sponsor who handles operations and transactions. |

| Investment Types | Investors can choose between equity, debt, or hybrid syndications, each with different risk profiles and income expectations. |

| Sponsor Importance | The sponsor’s investment in the deal aligns their interests with those of the investors, making it crucial to assess their track record and compensation structure. |

| Risk Awareness | Investors should understand market risks, liquidity issues, sponsor reliability, and potential capital call requirements before committing funds. |

Real Estate Syndication Explained in Plain Terms

Real estate syndication strips away complexity to answer a fundamental problem for investors: how do you buy the big deals? A commercial office tower, a 200-unit multifamily complex, or a high-value mixed-use development sits outside the reach of most individual investors. The acquisition price alone might be $15 million, $50 million, or higher. Syndication solves this through a straightforward principle. Multiple investors pool capital to purchase properties that would be impossible to buy alone. One lead player (the sponsor) orchestrates the entire transaction, while passive investors contribute money and receive their share of returns. Think of it as crowdfunding for real estate, except it’s structured with legal entities, clear governance, and defined investor protections.

The mechanics work through a simple partnership model. The sponsor identifies the opportunity, secures financing, completes due diligence, and manages the property post-acquisition. Limited partners provide the capital and remain passive. Typically structured as limited partnerships or LLCs, these arrangements distribute profits from three sources: ongoing cash flow from operations, property appreciation over the holding period, and net proceeds from the eventual sale. A sponsor manages acquisition and operations, while investors share risks and rewards proportionately based on their capital commitment. No investor bears unlimited liability, no partner gets bogged down in day-to-day management, and no single person carries the full weight of a deal that might take 18 months to execute. It works because each party focuses on what they do best. The sponsor applies operational expertise and market intelligence. Investors contribute capital and trust the process.

Here’s what makes this structure powerful for your portfolio. Syndication grants access to institutional-quality commercial real estate that typically demands millions in upfront capital and sophisticated operational knowledge. A typical investor might have $100,000 or $250,000 to deploy—enough to invest alongside others but not enough to acquire a trophy office building solo. Syndication lets that capital work harder. You gain exposure to larger assets, professional management, and diversified holdings across multiple properties and markets. For savvy investors closing deals with new approaches, syndication often provides better risk-adjusted returns than single-property ownership because the sponsor spreads risk across tenants, geographies, and asset classes. The sponsor absorbs the operational complexity—lease negotiations, tenant relations, maintenance coordination, capital expenditures. You collect cash distributions and track appreciation without managing phone calls at midnight.

Understanding the investor’s role matters. As a limited partner, you have zero control over operational decisions, no authority over tenant matters, and no voice in refinancing or sale timing. The sponsor controls those levers. Your contractual rights center on financial transparency, regular reporting, and proportional distribution of returns. Before committing capital, you review the offering memorandum, understand the deal’s assumptions (rent growth, expense management, exit strategy), and verify the sponsor’s track record. Some syndications return all profits to investors; others use a preferred return structure where investors receive their agreed percentage first, and the sponsor collects carried interest only after reaching a return threshold. The specifics vary, which is why reading the actual partnership agreement (not just the marketing materials) becomes non-negotiable.

Pro tip: Before joining any syndication, request the sponsor’s last three completed deals and speak directly with past investors about actual performance versus projected returns—marketing materials show potential, but investor conversations reveal reality.

Key Players and Structuring Models

Every real estate syndication has a distinct cast of characters, each playing a specific role. The sponsor (also called the general partner) sits at the center. This person or entity identifies the deal, structures the transaction, arranges financing, manages acquisitions, and runs daily operations. Sponsors typically invest their own capital alongside passive investors, which aligns their interests with yours. A sponsor with $500,000 of their own money in a $10 million deal thinks differently than one with zero skin in the game. Limited partners are the investors. You provide capital, receive distributions, and maintain a passive role. Your liability is capped at your investment amount. You cannot force decisions, override the sponsor’s judgment, or demand changes to operations. This separation of duties exists by design. The sponsor has operational expertise and market knowledge. You have capital to deploy. Both benefit when the deal succeeds.

The legal structure determines how profits flow, who bears liability, and how the partnership operates. Real estate syndications commonly use Limited Partnerships and LLCs as their backbone. A Limited Partnership includes a General Partner (the sponsor) with unlimited liability and limited partners (investors) with capped liability. An LLC offers flexibility and treats all members similarly unless the operating agreement specifies otherwise. Most modern syndications use LLCs because they provide flexibility in profit distribution and reduce complexity. The choice between structures depends on tax implications, liability preferences, and the sponsor’s preferences. Here’s the practical reality: the legal structure matters less than the operating agreement. That document defines everything: how profits distribute, when distributions occur, what happens if the sponsor exits, voting rights, and dispute resolution. Two syndications with identical LLC structures can operate completely differently based on their operating agreements.

Profit Distribution Models

Profit sharing typically follows one of two approaches. Waterfall structures distribute returns in tiers. Investors might receive 100 percent of cash flow until they hit an 8 percent preferred return, then profits split 70 percent to investors and 30 percent to the sponsor until investors achieve a 12 percent return, then profits split 50/50 thereafter. This incentivizes the sponsor to maximize returns because they only collect significant fees after investors reach predefined thresholds. Straight splits are simpler: if you invest 40 percent of the capital, you receive 40 percent of distributions. No preferred returns, no tiered structures, just proportional ownership. Waterfall models align sponsor and investor interests more effectively, though they require careful underwriting to understand what distributions you’ll actually receive at various performance levels.

Syndications can be equity-based, debt-based, or hybrid, depending on investment objectives. Equity syndications give you ownership in the property and ongoing cash flow plus appreciation. You win when the property appreciates and rents increase. Debt syndications involve lending to a sponsor or borrowing against a property. You receive interest payments and principal repayment, with fixed returns regardless of property performance. Hybrid structures combine both: you own a piece of the property and also hold a preferred return (like a debt instrument) before participating in further upside. Your choice depends on risk tolerance. Equity provides higher potential returns but carries more volatility. Debt provides stability but caps your upside. Most North American investor syndications skew equity because real estate investors want exposure to appreciation, not just interest income.

The sponsor’s skin in the game matters tremendously. Look for sponsors investing 5 percent, 10 percent, or more of their own capital. This commitment signals confidence in their own analysis. A sponsor with nothing invested can still prioritize themselves over investors through aggressive management fees or quick exits. Conversely, a sponsor who has $2 million of personal capital alongside yours thinks long-term. They sweat the same market fluctuations you do. When analyzing a syndication opportunity, compare sponsor compensation structures. Some charge acquisition fees (3 percent to 5 percent of the purchase price), asset management fees (0.5 percent to 1.5 percent of property value annually), and disposition fees (1 percent to 2 percent at sale). Others charge minimal fees but take carried interest (profit share) only after investors achieve returns. The structure reveals priorities. High upfront fees suggest the sponsor profits whether the deal succeeds or fails. Fee structures tied to performance alignment mean the sponsor only collects when you do.

Pro tip: Request a side-by-side comparison of the sponsor’s last three deals showing projected returns versus actual distributions received, then verify those numbers with past investors in those specific syndications.

Types: Equity, Debt, and Hybrid Syndications

Real estate syndications come in three flavors, and understanding the difference shapes your entire investment experience. Your choice determines your risk profile, return potential, and role in the deal. Equity syndications give you actual ownership in the property. You buy in at the acquisition, own your slice throughout the holding period, and benefit from two income streams: monthly cash flow from operations and property appreciation. If a multifamily property is acquired for $20 million and sells five years later for $28 million, equity investors share in that $8 million gain plus all the cash collected from rents minus expenses. You’re betting on the sponsor’s ability to increase rents, control costs, and exit profitably. Equity syndications typically target 12 percent to 20 percent annualized returns, though actual results depend entirely on market conditions and sponsor execution. The trade off: higher potential returns come with higher volatility. A market downturn affects your equity position immediately. Equity syndications offer ownership and participation in cash flow and appreciation, making them the most common structure among growth-focused North American investors.

Debt syndications flip the model entirely. Instead of owning the property, you lend money to the sponsor or against the property itself. You receive predetermined interest payments monthly or quarterly, regardless of how the property performs. If a sponsor borrows $5 million at 8 percent interest, you collect $400,000 annually whether rents skyrocket or decline. The sponsor’s property could double in value, but you still receive your 8 percent. This predictability has appeal. You know exactly what to expect. Your returns don’t fluctuate with market cycles. If the property appreciates significantly, you don’t participate. You collected your 8 percent while the sponsor and equity investors captured the upside. Debt syndications typically offer 6 percent to 10 percent annual returns, with significantly lower volatility than equity. The risk centers on sponsor execution and whether rental income covers the debt service. A struggling property might default, leaving you with a foreclosure process and potential losses. Debt syndications suit conservative investors seeking steady income over appreciation potential.

The Hybrid Advantage

Hybrid syndications split the difference and often represent the sweet spot for sophisticated investors. Hybrid financing combines debt and equity characteristics, providing fixed income with upside potential, balancing risk and returns effectively. A typical hybrid structure might guarantee you an 8 percent preferred return like debt, then give you 20 percent of profits above that threshold like equity. You receive stable cash flow regardless of performance, but if the deal crushes projections, you participate in outsized returns. Some hybrids use mezzanine financing, where your investment sits between the senior debt and equity. You get paid after the bank’s loan but before pure equity investors. This positioning offers better returns than debt with less volatility than pure equity. Another hybrid variant uses convertible structures: you start as a debt holder earning interest, then convert to equity ownership at a predetermined price if the deal performs well. This gives you downside protection (your interest payments continue regardless) while capturing upside if the property exceeds targets.

Choosing your syndication type requires honest assessment of your financial goals and risk tolerance. Equity syndications make sense if you have capital you won’t need for five to seven years, can stomach 20 percent annual fluctuations, and want exposure to real estate appreciation. You’re betting on sponsor competence and favorable market conditions. Debt syndications fit investors seeking passive income to supplement operations, those nearing retirement, or anyone building cash reserves. You sacrifice upside for predictability. Hybrids appeal to investors wanting both stability and participation, though they require deeper underwriting to model returns at various performance scenarios. Here’s the reality: most wealth accumulation in real estate comes from equity exposure and appreciation, not interest income. Equity syndications have generated the highest absolute returns over full market cycles. But debt syndications have protected capital during downturns and provided steady income when markets contracted. The best syndication for you depends on your specific situation, not industry trends. Some investors maintain a blended approach: 60 percent equity syndications for growth, 40 percent debt or hybrid for stability.

Here’s a breakdown of the primary syndication types and what each offers investors:

| Syndication Type | Ownership Structure | Income Source | Risk/Return Profile |

|---|---|---|---|

| Equity | Direct property share | Cash flow & appreciation | High return, higher risk |

| Debt | Loan to sponsor | Fixed interest payments | Moderate return, low risk |

| Hybrid | Debt and equity mix | Fixed plus bonus share | Balanced return, medium risk |

When evaluating any syndication, compare the return scenarios honestly. Request underwriting showing base case (most likely scenario), upside case (strong execution), and downside case (market pressure). Most marketing materials show base case assuming rent growth of 3 percent annually and expense discipline. Ask what happens if rents grow only 1 percent or decline in year three. A quality equity syndication still returns 10 percent in the downside scenario. A weak one craters below 5 percent. Debt syndications look attractive in marketing, but verify the underlying property generates enough income to cover interest payments with reasonable cushion. A debt syndication secured by a struggling asset is no safer than equity in that same asset.

Pro tip: Build a spreadsheet comparing three syndication opportunities side by side: projected cash flow by year, preferred return structure, sponsor fees at each stage, projected exit timing, and most importantly, sponsor compensation tied to reaching stated returns versus collected upfront regardless of performance.

Step-by-Step Deal Process and Payouts

A real estate syndication unfolds in distinct phases, each with specific investor touchpoints and payout mechanics. Understanding this timeline helps you manage expectations and know when to expect distributions. Phase 1: Deal Sourcing and Due Diligence begins when the sponsor identifies a property. The sponsor analyzes market conditions, property financials, lease agreements, tenant quality, and exit scenarios. This phase can last 30 to 90 days. During this time, you don’t exist yet as an investor in this specific deal. The sponsor is vetting whether the opportunity makes sense at all. A sponsor might evaluate 50 properties to syndicate one. Phase 2 involves creating offering documents. The sponsor works with legal counsel to draft the operating agreement, private placement memorandum, subscription agreements, and financial projections. This documentation defines your rights, return expectations, fee structure, and exit timeline. You’ll receive these materials before being asked to commit capital. Read them carefully. This is your contract, not marketing material.

Phase 3: Capital Raising brings you into the picture. The sponsor markets the syndication to accredited investors and those meeting suitability requirements. Typically this lasts 60 to 120 days. You submit your subscription agreement, conduct due diligence on the sponsor and property, and wire capital. The sponsor continues raising capital until reaching their target, which might be $5 million, $10 million, or more. Once the funding closes, the capital is locked. You cannot withdraw. Phase 4 is acquisition. The sponsor sources and underwrites the deal, then acquires the property, often within 45 to 90 days of closing the capital raise. This is when your money actually deploys. Before acquisition, your capital sits in escrow. Some sponsors charge acquisition fees at this point, deducting 3 percent to 5 percent of purchase price from investor capital before deploying it. Your $100,000 investment might become $95,000 deployed if acquisition fees are 5 percent. During acquisition, the sponsor arranges institutional financing (typically 65 percent to 75 percent of purchase price), uses investor equity for the remainder, and closes on the property.

The Operating and Payout Phase

Phase 5 spans the majority of the holding period, often five to seven years. The sponsor manages the property, collects rents, pays expenses, and distributes cash to investors. This is where payouts materialize. Payouts typically follow preferred return thresholds and profit splits based on waterfall structures, with distributions sent quarterly or semi-annually. If the syndication projects a preferred return of 8 percent annually on your $100,000 investment, you should receive approximately $2,000 quarterly ($8,000 annually). That distribution comes from cash the property generates after expenses and debt service. If the property underperforms and cash flow is tight, distributions might be delayed or reduced. Some months the sponsor holds capital for capital expenditures (roof repairs, parking lot resurfacing). This reduces distributions temporarily but preserves property value. You receive quarterly reports showing rental income, operating expenses, debt service, and remaining cash available for distribution. Review these reports. They tell you whether the deal tracks projections or diverges. A property projecting $1.2 million annual rent growth that delivers only $800,000 signals performance issues.

Phase 6 is exit and final payout. At the syndication’s maturity (five years, seven years, or whenever the sponsor originally planned), the sponsor either refinances the property, sells it, or continues holding. Most syndications exit via sale. The sponsor markets the property, negotiates with buyers, and closes the transaction. Upon sale, all investors receive their capital back plus accumulated profits. The payout sequence matters. If you invested $100,000 and the waterfall specifies a preferred return of 8 percent annually, you receive that back first. Only after all investors recoup their preferred return does the sponsor collect carried interest or additional profit shares. Here’s the practical reality: when a property sells after five years for a 15 percent total return, your actual distribution depends entirely on when returns were distributed during holding and whether sale proceeds exceed or fall short of projections. A property that returned 6 percent annually ($30,000 profit over five years) plus 9 percent from sale proceeds ($9,000) yields 15 percent total. A property that returned 0 percent annually but 15 percent at sale also yields 15 percent total, but cash flow during those five years disappeared. The timing and predictability of distributions matter as much as total returns.

Taxation enters the picture immediately. Real estate syndications generate K-1 forms showing your share of taxable income, regardless of whether you received cash distributions that year. A property with strong cash flow might distribute $8,000 annually to you but generate $12,000 in taxable income you owe taxes on (the difference is depreciation deductions not paid in cash). You’ll need an accountant familiar with real estate syndications to optimize reporting. Depreciation benefits syndication investors substantially. Over 27.5 years, a $1 million residential property depreciates approximately $36,000 annually. That depreciation offsets taxable income without requiring actual cash outlay. Many syndications distribute less cash than they generate in taxable income specifically to take advantage of depreciation sheltering. This is legitimate tax planning, not tax evasion. Understanding it prevents surprise tax bills in April.

Pro tip: Before committing capital, request a sample K-1 form from the sponsor’s previous syndications and discuss tax implications with your accountant, who can model your specific tax situation and confirm the syndication’s structure aligns with your overall investment strategy.

Legal Framework, Disclosure, and Compliance Rules

Real estate syndications operate within a strict regulatory framework that exists to protect investors and ensure sponsors operate with integrity. This framework is not bureaucratic overhead—it’s fundamental infrastructure. When a sponsor follows compliance rules properly, you have recourse if something goes wrong. When they cut corners, you have almost none. Understanding these rules helps you identify trustworthy sponsors and recognize red flags. Real estate syndications are securities. This classification matters enormously. A securities offering must comply with federal regulations (primarily the Securities Act of 1933 and Securities Exchange Act of 1934) and state securities laws in every state where investors reside. Real estate syndications are securities offerings regulated under federal and state securities laws, requiring compliance with Regulation D exemptions and disclosure obligations. The Securities and Exchange Commission does not approve syndications before they launch. Instead, sponsors must qualify for specific exemptions allowing them to raise capital from private investors without full SEC registration. Regulation D (often called “Reg D”) provides these exemptions. The most common is Rule 506(b), which allows sponsors to raise unlimited capital from accredited investors plus up to 35 non-accredited investors. Rule 506© permits unlimited capital from accredited investors only, with stricter verification requirements. The distinction matters. If a syndication operates under Rule 506©, every investor must be accredited. If it’s Rule 506(b), the sponsor can include a few non-accredited investors, though this rarely happens.

Accreditation is the gatekeeper. An accredited investor meets specific financial thresholds: $200,000 annual income (or $300,000 for couples) for the past two years with reasonable expectation to continue, or $1 million net worth excluding primary residence. These thresholds exist because regulators assume wealthier investors can absorb losses and conduct adequate due diligence. They’re also controversial—many argue they exclude capable investors for arbitrary reasons. Regardless, most North American syndications require accreditation. Some sponsors use the “bad actor” disqualification rule, which bars certain people (those convicted of fraud, for example) from offering securities. This protects investors by preventing known bad actors from syndication activities. When evaluating a sponsor, verify they have no disqualification history through FINRA (Financial Industry Regulatory Authority) databases or SEC records. Disclosure requirements are extensive. The sponsor must provide a Private Placement Memorandum (PPM) before you commit capital. The PPM describes the investment opportunity, risks, sponsor background, financial projections, fee structure, conflicts of interest, and exit strategy. Comprehensive disclosure of risks through documents like the PPM is required, along with clear outlining of exit strategies and conflicts of interest. This document can run 50 to 100 pages. Read it thoroughly. It contains legal disclaimers, risk factors, and terms defining your rights. The PPM is binding. If the sponsor violates terms in the PPM or makes material misrepresentations, you have grounds for legal action. Many investors skip the PPM and rely on marketing materials or sponsor conversations. This is a mistake. Marketing materials highlight strengths. The PPM reveals weaknesses, risks, and limitations.

Key Compliance Obligations

Sponsors bear specific ongoing obligations after raising capital. They must maintain accurate records of all investor communications, maintain segregated bank accounts for investor funds, file state securities registrations or claim exemptions in each state where investors reside, and provide regular financial reporting and K-1 forms for tax purposes. They cannot commingle investor funds with personal funds or other business accounts. They cannot make material misrepresentations or omit material facts. They cannot change terms without investor consent. If a sponsor promises a preferred return of 8 percent and later reduces it to 6 percent, that’s a material change requiring amendment and investor approval. Most sponsors also maintain errors and omissions insurance, fidelity bonds, and other protections. These are not required by law but signal professionalism and reduce investor risk. Anti-fraud provisions apply regardless of exemption used. Under Rule 10b-5, sponsors cannot engage in fraud or deceptive practices. This includes false statements, material omissions, and engaging in deceptive schemes. Penalties for violations range from civil liability (paying back investors plus damages) to criminal prosecution (fines and imprisonment). The SEC and state regulators actively investigate syndication fraud. From 2015 to 2023, the SEC prosecuted dozens of real estate syndication fraud cases annually, with settlements averaging $5 million to $50 million. State regulators prosecute additional cases. This enforcement activity demonstrates that compliance matters. Sponsors who cut corners risk criminal charges and investors risk losing everything.

State-level compliance adds complexity. Each state requires syndications to register or claim exemptions before offering securities to residents. California, Texas, New York, and Florida have strict oversight. Some states require more detailed disclosures or impose additional investor protections. A sponsor must track these requirements and ensure compliance in every state. Failure to register properly can result in state regulatory action, forced rescission of offerings, and civil penalties. From an investor perspective, if you receive a syndication offering without proper state registration or exemption documentation, that’s a warning sign. A legitimate sponsor provides proof of compliance proactively. Your due diligence checklist should include verifying the sponsor has proper accreditation history, requesting the full PPM and reviewing it thoroughly, confirming the syndication is registered or exempted in your state, verifying the sponsor maintains proper insurance and bonding, and requesting references from past investors in specific syndications (not just a list of satisfied clients). Ask past investors: Did distributions arrive on schedule? Were quarterly reports detailed and accurate? How did the sponsor handle unexpected challenges? Did they communicate transparently or hide problems? These conversations reveal whether compliance extends from legal formality to operational practice. A sponsor complying with every regulation on paper but deceiving investors about property performance through selective reporting is still problematic. The legal framework creates structure and accountability, but your personal due diligence remains essential.

Pro tip: Request the sponsor’s state registration documents and SEC filings for their past three syndications, then verify those filings with the relevant state secretary of state and SEC websites to confirm accurate compliance history before committing capital.

Risks, Common Pitfalls, and Exit Considerations

Real estate syndications carry genuine risks that deserve serious consideration before you commit capital. The risks are not theoretical or unlikely. They materialize regularly in markets across North America. Understanding them positions you to avoid catastrophic mistakes and recognize when a syndication presents unacceptable downside. Market risk sits at the foundation. A property acquired during favorable conditions can deteriorate rapidly when markets shift. Interest rates spike, unemployment rises, or a major employer leaves the region. Vacancy increases, rents stagnate, and the property’s value declines. An equity syndication projecting 12 percent returns can easily deliver 4 percent or negative returns in adverse scenarios. This risk is unavoidable. Even the best sponsors cannot control macroeconomic cycles. What they can control is their response. Do they maintain adequate reserves? Do they communicate honestly when challenges emerge? Do they adjust operations intelligently or stick stubbornly to original projections? Sponsor risk is more troubling because it involves human factors. A sponsor might lack experience despite claiming expertise. A sponsor might prioritize their own compensation over investor returns. A sponsor might make reckless operational decisions or engage in outright fraud. Common pitfalls in real estate syndication investing include failing to research the sponsor’s track record, misunderstanding deal structures and fees, and ignoring market fundamentals. This research is non-negotiable. Request detailed information about every property the sponsor has previously syndicated. Ask about projects that underperformed or failed. Sponsors will highlight successes. Your job is uncovering the full picture. A sponsor who syndicated ten properties should be able to describe all ten in detail, including those that disappointed. Evasiveness is a warning signal.

Liquidity and Exit Risk

Liquidity risk deserves special attention. Your syndication investment is typically illiquid. You cannot sell your position on a secondary market like you can sell public stocks. You are locked in until the sponsor executes the exit (usually a property sale after five to seven years). If circumstances change and you need capital urgently, you cannot access it easily. Some syndications create secondary markets where investors can trade positions, but these markets are thin and buyers demand significant discounts. You might own a position worth $100,000 based on the property’s current valuation but only find a buyer willing to pay $75,000. This illiquidity premium is substantial. Investors should only commit capital they can afford to have locked away for the full holding period. Exit risk encompasses the challenge of successfully selling or refinancing the property at the anticipated time. A sponsor projects exiting a property in year five. But what if market conditions deteriorate and selling at that time results in a loss? Does the sponsor hold longer? Do they accept below-market pricing? Do they refinance instead? These decisions profoundly affect your returns. Exit timing risk becomes acute during market downturns. A sponsor might hold a property through a cycle, hoping for recovery, extending your investment timeline beyond original plans. You remain invested longer than anticipated with capital generating lower returns. Alternatively, a sponsor might force a sale during unfavorable conditions to exit on schedule, crystallizing losses. Neither outcome is ideal. The best sponsors maintain flexibility and communicate transparently about exit timing, adjusting strategies as conditions warrant rather than adhering rigidly to original projections.

Capital call risk surprises unprepared investors. Many syndication agreements include capital call provisions allowing sponsors to request additional capital from investors for unforeseen capital expenditures. A roof failure, major system replacement, or structural damage might trigger a capital call. Investors who committed initial capital without budgeting for potential additional contributions face difficult choices: contribute more capital or lose their existing investment through dilution. Before investing, clarify whether the syndication includes capital call provisions and estimate the likelihood of calls based on property age and condition. Overleverage risk compounds when sponsors use excessive debt financing. A property financed at 75 percent debt is stable with reasonable cash flow. A property financed at 85 percent debt becomes vulnerable to minor cash flow disruptions. If rents decline slightly or expenses increase unexpectedly, the property might struggle to cover debt service. Lenders might demand principal paydown or force refinancing at worse terms. A severely overleveraged property can default even if the property itself is sound. When evaluating a syndication, examine the loan-to-value ratio (LTV) carefully. LTVs above 80 percent introduce meaningful refinance risk. LTVs above 85 percent are aggressive and suitable only for experienced investors understanding the consequences.

Consider the main risks and how they could impact your investment in syndications:

| Risk Type | Example Scenario | Potential Investor Impact |

|---|---|---|

| Market Risk | Rent declines, high vacancies | Lower returns or loss of capital |

| Sponsor Risk | Inexperienced or misaligned sponsor | Poor execution or possible fraud |

| Liquidity Risk | No buyer for your position | Funds locked for several years |

| Capital Call Risk | Major repair needs extra funding | Need to invest more or face dilution |

Realistic Exit Expectations

Understanding exit mechanisms prevents disappointment. Most syndications exit via property sale. The sponsor markets the property, negotiates with qualified buyers, and completes a transaction. The typical timeline is month 50 to month 72 of a five to seven year hold, though this varies. Some syndications refinance instead of selling, converting investor equity into a new loan and returning capital while maintaining the investment. Refinance exits usually occur when property values have appreciated substantially and refinancing rates offer favorable terms. A refinance exit is attractive because investors recover capital (allowing redeployment) while maintaining upside if they choose. Some sponsors include put options giving investors the right to force a sale or redemption at a specified time if the sponsor fails to exit. Put options exist to protect investors from sponsors extending holds indefinitely. However, put option terms vary dramatically. Some are truly protective. Others include restrictions making them effectively worthless. When reviewing a syndication, examine exit provisions carefully. A clear exit date with defined consequences if the sponsor misses it provides more certainty than vague language suggesting “approximately” a certain timeline.

Your role during the exit phase is oversight. As distributions approach the final payout, scrutinize the sale process. Are comparable sales support the asking price? Is the sponsor marketing the property aggressively or accepting the first offer? Are buyer contingencies reasonable or heavily weighted toward the buyer? A sponsor might negotiate aggressively or accept marginal offers depending on their own interests. Your capital return should not subsidize sponsor mistakes. If a property projected to sell for $25 million gets offloaded for $22 million due to poor negotiation, that $3 million difference comes from investor returns. Questions to ask your sponsor as exit approaches: What is the current market for comparable properties? What are the specific terms of the leading offer? How does this compare to your original underwriting? What risks exist in closing on timeline? These questions signal you are engaged and monitoring their performance.

Pro tip: Before committing capital, request a detailed breakdown of the syndication’s downside scenario showing what happens if the property depreciates 15 percent, then compare the projected loss to your ability to absorb it without jeopardizing your overall financial plan.

Unlock the Power of Real Estate Syndication with Expert Partnership

Real estate syndication offers a unique path to access large-scale deals and attractive returns but comes with challenges like complex deal structuring, rigorous due diligence, and managing multi-layered investor relationships. If you are ready to step beyond the frustrations of navigating complicated partnerships and want to maximize your profits with confidence, exploring specialized support can transform your investment journey. The article highlights critical pain points such as aligning sponsor interests, understanding waterfall structures, and ensuring clear exit strategies — all areas where a seasoned partner adds immense value.

At Sims Ventures, we go beyond capital by providing strategic advisory alongside tailored financing solutions to help you conquer these challenges. Whether you need assistance with structuring entities, negotiating contracts, or optimizing deal and capital structuring, our expertise is designed to keep your ventures on track and your risks managed effectively. Discover how our comprehensive services bring clarity and control to your investments so you focus on growth while we handle the complexity.

Explore more about how to Maximize Your Real Estate Investment Profits with our proven solutions.

Take control of your next real estate syndication with Sims Ventures. Visit us at https://simsventures.com to learn how our partnership approach empowers investors like you to unlock bigger deals through smarter financing and strategic execution. Act now to transform your syndication experience into predictable success.

Frequently Asked Questions

What is real estate syndication?

Real estate syndication is a method where multiple investors pool their capital to acquire larger investment properties that would be out of reach for individual investors. A lead sponsor manages the entire process while passive investors provide the funding.

What are the key roles in a real estate syndication?

The key roles in a real estate syndication include the sponsor (or general partner), who manages the deal and operations, and the limited partners (investors), who provide capital and receive returns without engaging in day-to-day management.

How are profits typically distributed in real estate syndications?

Profits in real estate syndications are usually distributed based on either a waterfall structure, where returns are tiered, or a straight split model, where investors receive profits proportionate to their investment. This ensures alignment between the sponsor’s and investors’ interests.

What are the risks associated with real estate syndication investments?

The risks of real estate syndication include market risk, where property valuations can decline, sponsor risk related to the experience and integrity of the sponsor, liquidity risk from the illiquid nature of investments, and potential capital calls for unforeseen expenses.

{kind=link}